2023 Biologics & Advanced Therapies Contract Manufacturing Report by Alira Health

In recent years, Biologics and Advanced Therapies (ATs) have emerged as the primary drivers of innovation within the pharmaceutical industry.

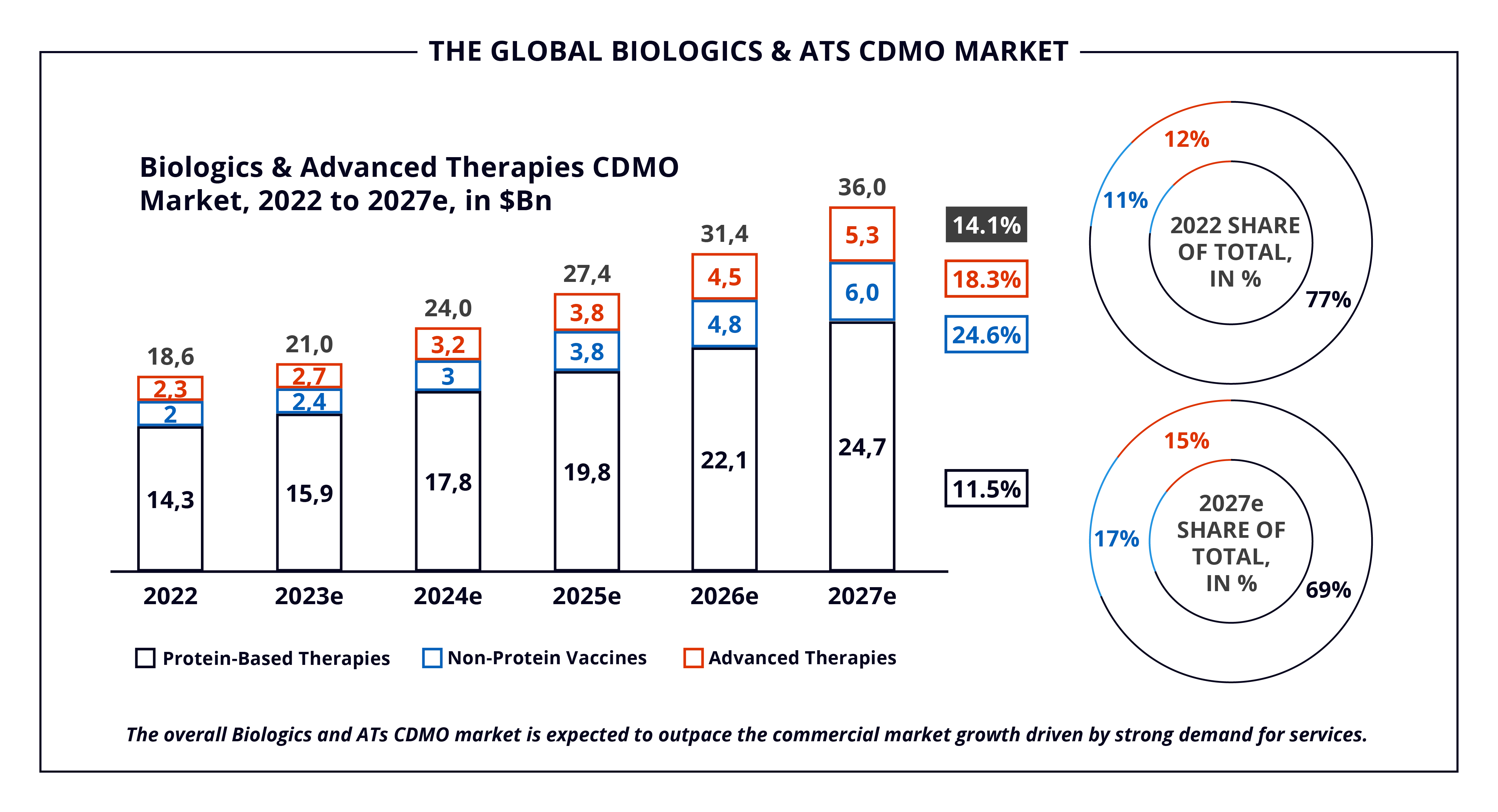

As Biologics and ATs explode in demand, the Biologics and ATs Contract Development and Manufacturing Organization (CDMO) market is projected to witness robust growth. As captured in Alira Health’s 2023 Biologics & Advanced Therapies Contract Manufacturing Report, the market will escalate from $18.6B to $36.0B from 2022 to 2027, at a Compound Annual Growth Rate (CAGR) of 14.1%. This expected growth is leading major CDMOs to invest significantly to scale up capacity and adapt manufacturing processes. Keep reading for an overview of the Biologics and ATs CDMO landscape.

Note that all data are from Alira Health’s “2023 Biologics & Advanced Therapies Contract Manufacturing Report.”

Global Biologics and ATs CDMO Market

The increased demand for Biologics and ATs along with the rise in research and development (R&D) funding are strong drivers for the CDMO industry.

The estimated value of the Biologics and ATs CDMO market is $18.6B in 2022, with an expected growth at a CAGR of 14.1%, reaching $36B by 2027. The growth is propelled by increasing demand in all three major segments of this market (protein-based therapies, non-protein vaccines, and ATs). Specifically, the last two segments combined will showcase the highest growth and are on track to constitute 32% of the total market by 2027, up from 23% today.

The protein-based therapies segment is expected to grow at an 11.5% CAGR from 2022 to 2027, while the largest market growth is driven by non-protein vaccines and ATs, projected to grow 24.6% and 18.3%, respectively.

As a result of this impressive market growth, CDMOs aspiring to lead in Biologics and ATs manufacturing are venturing into the integration of technologies capable of addressing the evolving landscape.

The CDMO landscape is rich in opportunities, including that presented by patent expiration and the rise of biosimilars. CDMOs can support biosimilar manufacturers by providing rapid turnaround and lower manufacturing costs while ensuring supply chain flexibility.

Another opportunity is that demand for ATs is outstripping manufacturing capacities. CDMOs provide ATs sponsors with the critical capacity and quality necessary to make them successful. Additionally, the complexity of manufacturing cell therapy products creates major opportunities for CDMOs, which can supply sponsors with deep domain expertise and robust process development capabilities. Sponsors of Biologics and ATs products will increasingly seek CDMOs as external manufacturing partners to increase production, optimize capacity, reduce costs, and create a secure supply chain.

Large CDMOs Dominate the Market but Small/Micro Drive Innovation

Eight large CDMOs dominate the greatest share at 65.2% of the global market and 65% of total revenue for the CDMO market. Currently, medium-sized players contribute 25%; large and medium players combined represent nearly 90% of the total revenue.

Although small and micro manufacturers still represent the smallest contributor to the global outsourcing output with a 10.9% share of the market, mainly due to capacity constraints, they will drive the industry’s innovation and consolidation activity in the coming years. Such fragmentation represents a large pool of acquisition targets for private equity and strategic investors.

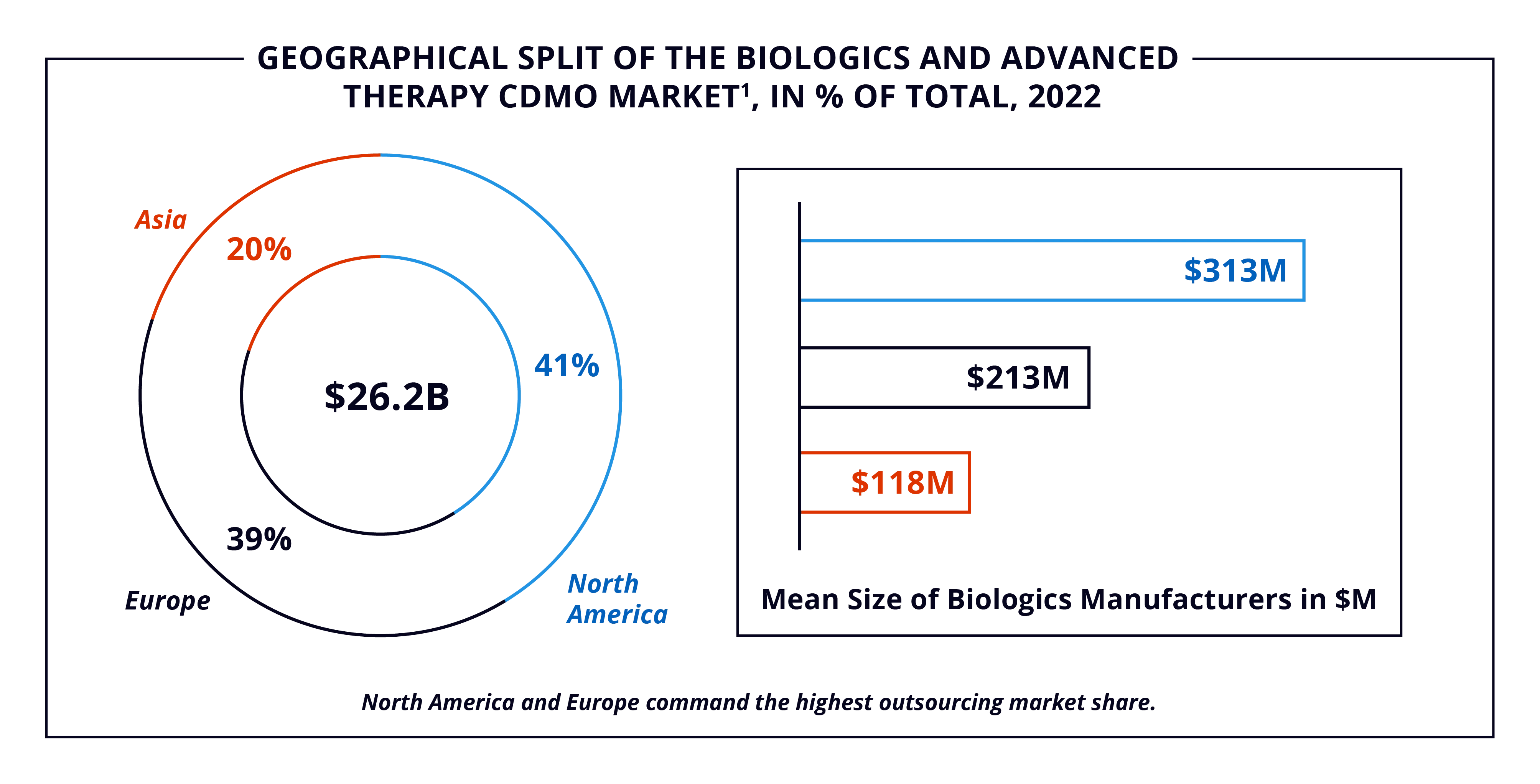

Geographically, the two main global regions for biologics and ATs manufacturing are North America and Europe, the headquarters for eight of the top ten CDMOs. However, the APAC region is expected to increase its importance in the coming years due to biosimilar innovation and widespread adoption.

Biologics and ATs Therapies Market Trends

Due to intensive R&D efforts and breakthroughs in expression systems and manufacturing techniques, the Biologics and ATs market has experienced substantial growth. The 2022 biologics and ATs market was dominated by protein-based biologics, representing 86.2% of the market ($376B), followed by vaccines comprising 13% ($58B) and ATs representing less than 0.5% ($2B).

COVID-19 vaccines development and launch impacted the Biologics and ATs landscape, promoting the regulatory approval of non-COVID-19-related innovative therapies. Regardless of pandemic-related challenges, biopharmaceuticals thrived in 2020-21. The success of COVID-19 Biologics and ATs continued to drive investments in R&D and is projected to promote a significant $281B growth in the market from 2022 to 2027. Due to their widespread adoption, protein-based biologics will retain the lead with 80% of the market, while ATs are expected to grow to 9%.

Biologics and ATs Innovative Pipeline

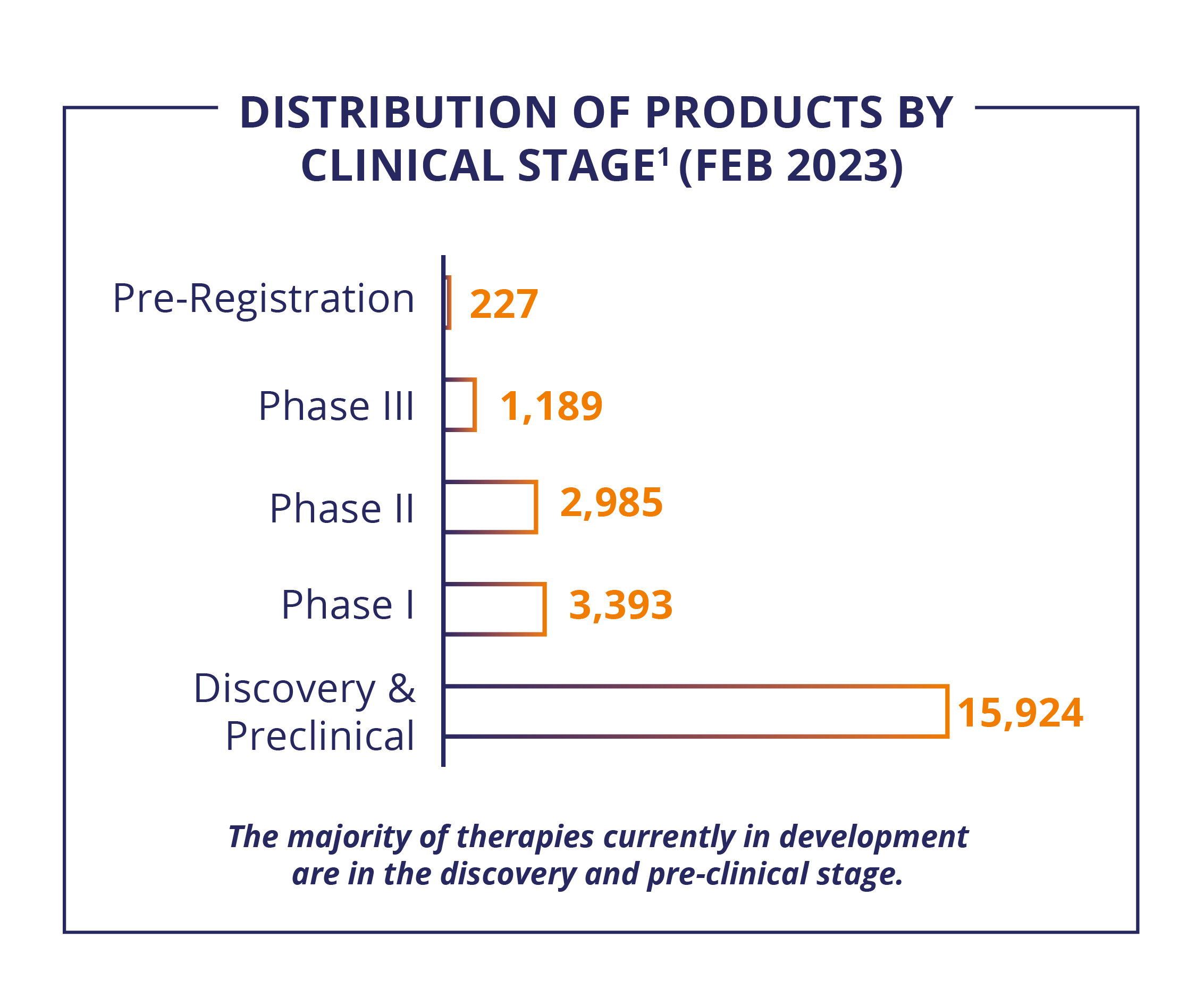

The deep innovation pipeline for Biologics and ATs includes almost 24,000 therapies in development, with early developmental assets making up 67%. Remarkably, half of the pipeline is antibodies and cell and gene therapy products. Oncology arises as the main therapeutic area, with an outstanding pipeline of 9,000 pipeline products.

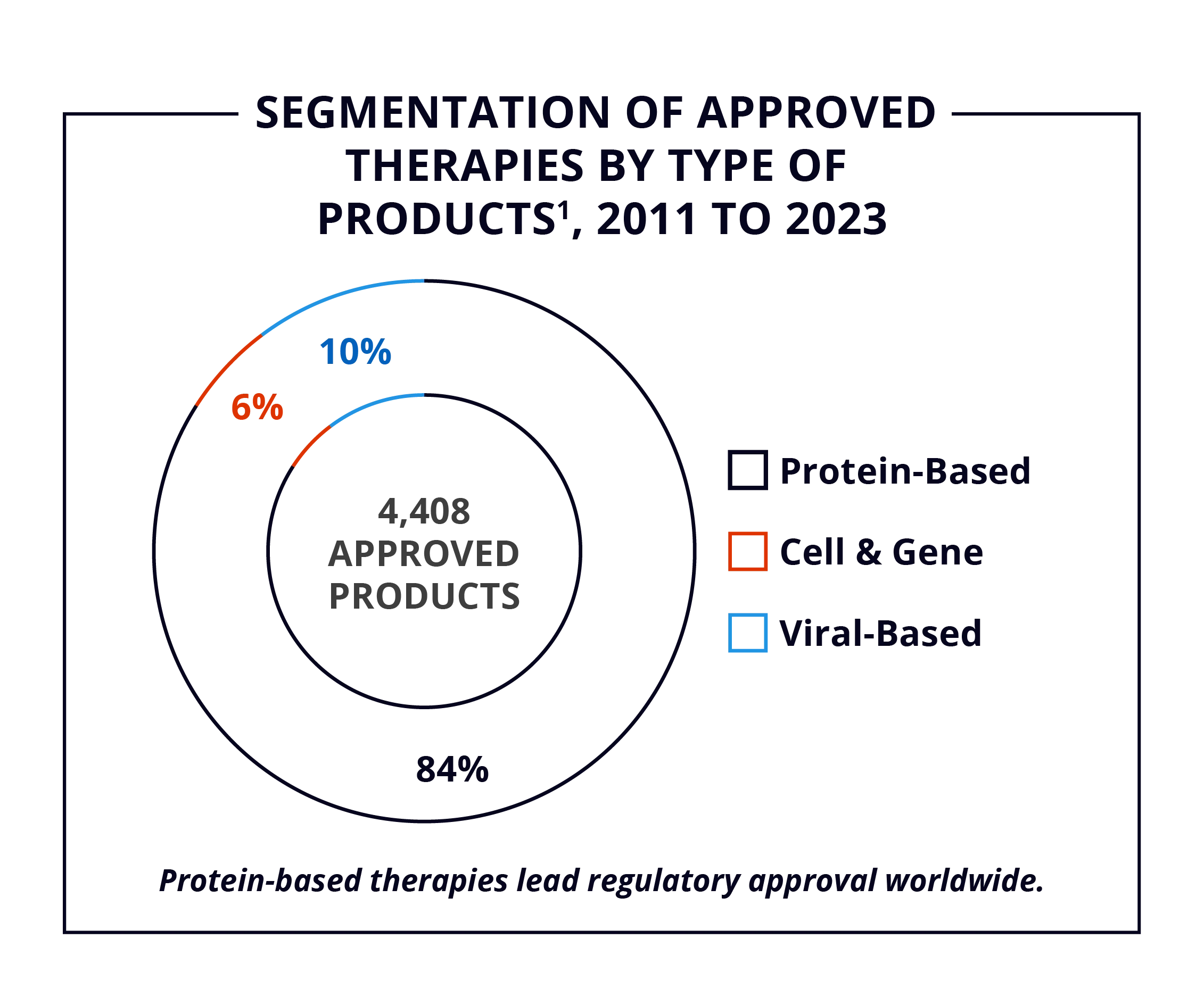

From 2011 to 2023, over four thousand Biologics and ATs secured regulatory approval worldwide,1 with protein-based therapies accounting for 84% of approvals. North America leads Biologics and ATs development at 14%, followed by China at 10%. The EU+UK, India, and Japan hold 20% of the market as of 2023.

Learn more, including an in-depth market analysis and examination of transactional activity within Biologics and ATs CDMO space, by downloading Alira Health’s 2023 Biologics & Advanced Therapies Contract Manufacturing Report.

1Represents all drugs present in all global markets, with each single-country approval accounting for one unit